9. Synchrony Financial: Preferred Choice

Analysis that preceded one of my latest investments.

Investing in preferred stock is not something I frequently do. However, in rare occasions, investments in preferred issues can meet requirements of sound investment, even with all the disadvantages compared to comparable common equity or bond investment.

Investment thesis

Prospect considered here are series A preferred shares of Synchrony Financial SYF 0.00%↑ , one of the largest credit card lending banks in the USA. I wrote about Synchrony here and what I think about it as a bank and a business. The purpose of this post is to focus its preferred issue.

In short, Synchrony Financial can be described as one of the larger credit card lending banks in the USA, accounting for roughly 10% of the outstanding credit card balance in the USA. They operate under a simple and concentrated business model, which results in extraordinary profitability for a bank, but carries a risk as in case of any business with concentrated product base. Contrary to the standard retail banking model, Synchrony has forgone the approach of having its own predominantly physical distribution channels. Opposed to having a vast network of branches, it offers mostly credit cards through retail branches of large consumer chains, or online in partnerships with large online consumer companies. In turn, this approach leads to a low cost to income ratio, and, in long-term, above-average return on invested equity.

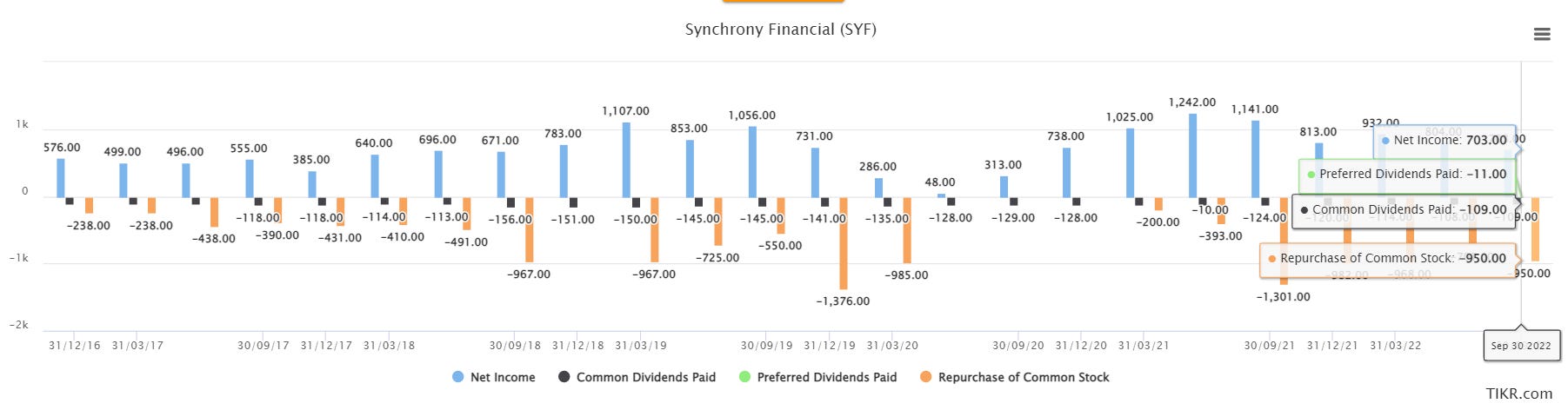

Since its listing, Synchrony had an outstanding record of return on equity, but also shareholder value creation, having almost returned in full the initial shareholder’s investment through buybacks and dividends. Within the whole operation, its preferred issue in only a marginal component when measured relative to the overall capital structure and earning power. Issue at mention (NYSE: SYF-PA), is most likely to be redeemed in November 2024 at USD 25 per share, implying a total annual compounding yield close to 22% at current price levels.

Preferred issue properties

Synchrony issued its non-cumulative perpetual preferred shares in November 2019 for the of USD 734 million. In total, 30 million shares were issued at an average price of USD 24.67 per share, with declared dividend of USD 1.41 per (5.625% rate on par) year payable quarterly since February 2020. Issue is redeemable as of November 15, 2024 at 25 per share call price. This turned out to be a good timing for Synchrony, as it increased their Core Tier 1 Capital ratio right before the March 2020 crisis.

Reasoning for this specific issue were probably much different at the time, and it most likely had two major drivers.

At first, the basic reason banks would issue non-cumulative vs cumulative preferred shares is that from a regulatory point of view, non-cumulative preferred shares can be treated as common equity when calculating Core Tier 1 (CT1) capital adequacy ratio. If a cumulative share were issued, they would still count toward Tier 2 ratio, which includes supplementary capital elements which are considered less secure. Although this might be confusing, as cumulative property is viewed as a protection mechanism for investors, here security is defined from a point of view of the bank and banking system. In case of adverse conditions in banking industry and non-cumulative issues, banks have an option to avoid additional costs which would drain their capital reserves when they are needed the most.

Although not much was stated on the reason of the preferred shares issue, my guess it was that it was done to pre-empt the impact of CECL adjustments that were expected to be fully implemented by 2021 at the time. Additional capital collected this way would give time to Synchrony to gradually increase its loan loss allowance (negative equity item) to then estimated level of USD 10.3 billion, while maintaining its buyback and dividend program intact.

Below is an extract from Q3 2019 earnings call explaining some reasoning behind this issue.

Before I provide details on our capital position, it should be noted that we elected to take the benefit of the transition rules issued by the joint federal banking agencies in March, which has 2 primary benefits. First, it delays the effect of the transition adjustment for an incremental 2 years; and second, allows for a portion of the current period provisioning under CECL to be deferred and amortized with the transition adjustment. With this framework, we ended the quarter at 15.8% CET1 under the CECL transition rules, 130 basis points above last year's level of 14.5%. The Tier 1 ratio was 16.7% under the CECL transition rules compared to 14.5% last year, reflecting the preferred stock issuance last November.

The total capital ratio increased 230 basis points as well to 18.1%, also reflecting the preferred issuance. And the Tier 1 capital plus reserve ratio on a fully phased-in basis increased to 27.3% compared to 20.7% last year, reflecting the increase in reserves as a result of implementing CECL and the preferred stock issuance. During the quarter, we paid a common stock dividend of $0.22 per share. Earlier this year, we announced that given the current economic uncertainty and being as prudent as possible, we made the decision to halt further share repurchases until we have greater visibility on the magnitude and the impact COVID-19 will ultimately have in the economic environment. We will continue to evaluate this as we move forward.

~Q3 2019 Earnings call

However, faith would have it differently, and Synchrony had to increase its loan loss allowances for almost complete the required amount of Q1 2020, to the levels required by CECL adjustments. Months later, gradual release of in allowances occurred, however they were stabilized close to the level expected at the end of 2024 for the similar sized portfolio.

At the same time, Q1 2020, the regulator granted an option to all banks to extend this gradual phase in period of additional loan loss allowances for an additional 3 years, until December 31, 2024.

~2021 10K, page 55

The combination of the two previous developments, formation of above expected loan loss reserves, and extension of regulatory deadline to fully phase in CECL has effectively allowed Synchrony to manage its equity with more freedom.

Synchrony now operates at historically high proportion of allowances to total loans.

For comparison, following FRED data shows series which could indicate what is in store for Synchrony in case of severe recession.

In hypothetical case of non-performing loans rising to 7%, accompanied by charge off rate of 11%, joint impact would be a negative before tax of 7%*11%* USD 86,012 million (gross loans outstanding in Q3 2022), or USD 663 million per year (compared to an average quarterly net income between USD 400 and USD 600 million). Amount more than covered by current provisions. One should always keep in mind just how much has regulation put a burden on the banking system since 2007 in order to keep it robust.

In the meantime, since the end of 2020, Synchrony also managed to stabilize their Tier 1 capital ratio and return USD 7.8 billion though buybacks and regular dividends to its shareholders, and additional USD 116 million though dividends on preferred issue. In total, more than 10x of equity collected though preferred issue was returned voluntarily since.

As for the preffered issue on its own, since the issuance of the 750,000 SYF-PA in Q4 2019, Synchrony has been paying quarterly dividend on it in the amount of USD ~11 million per quarter, or 42 million per year. Amount insignificant compared to its earning power and dividend and buyback cash use.

Given its authorized USD 2.8 billion stock repurchase plan until June 2023, it is conceivable that a similar plan will be redirected to preferred shares as of November 2024. Impact of repurchase of preferred shares on common equity Tier 1 ration is however higher than the same amount repurchase of common stock, which trade at higher price to book ratio. However, preferred repurchase would also lower funding costs (close to 5.7% since origination). If Synchrony is not in dire need for regulatory capital, it would be in the position of being able to fund the preferred issue repurchase with any type of debt costing up to 7.4% pre-tax (based on 5.7% after tax cost of dividends and 23% effective tax rate). Given its current BBB- rating on unsecured debt, it is more than realistic to assume that this capital can be collected at lower pre-tax cost than 7.4% (debt raise or aggressive deposit raise to fund more expensive preferred share redemption).

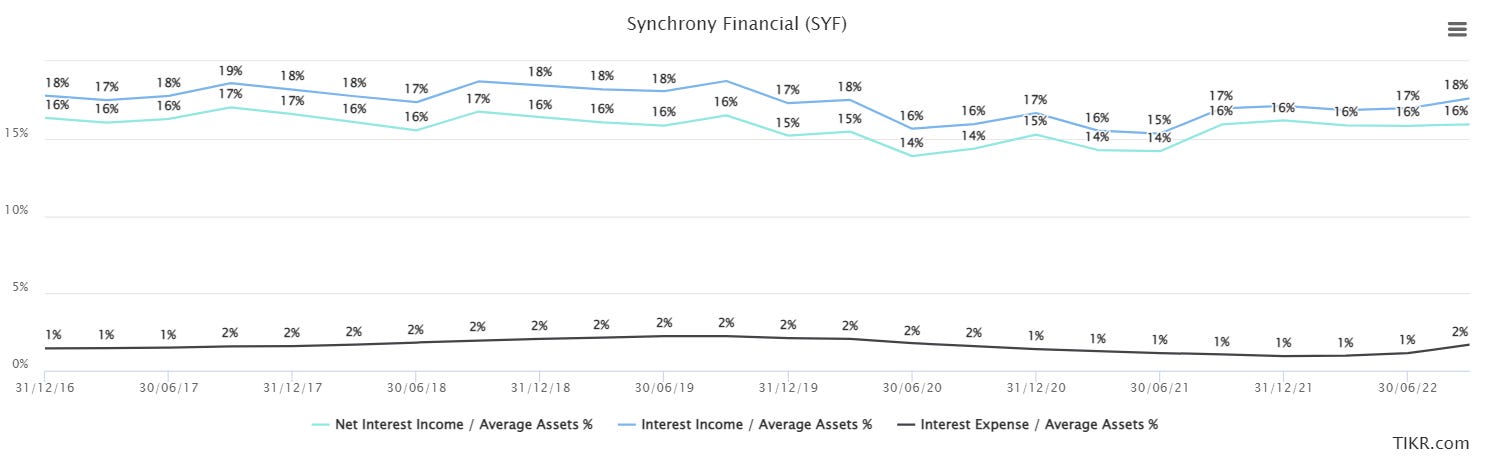

As I mention, for more comprehensive analysis of its banking business, my article on Synchrony provides more details, but it should be kept in mind that although Synchrony runs a concentrated, predominantly credit card potfolio, it does so for a good reason. Three exibits below, taken from the lates quarterly filings and TIKR overview, show what is a normal interest income and cost on its assets and liabilities.

In normal times, Synchrony is building its capital base quite agressivly with more then 15% interest rate spread. It is up to them then to alocate these funds either to fund future portfolio growth and by keeping it as an item in their regulatory capital, or return it to its shareholders. Together with this, Synchrony operates as a flexible operaion, with relatively low staff expenses for a normal bank and efficiency ration bellow 40%. This is mainly because they have mostly outsourced their underwriting to their retail paartners. But what this means is that in he case of reduction in lending due to recession, their relative net ineterest income after staff exenses will not decrease proportionaly to the reduction in its asset base. Their bottom line is flexible, and there is some level of robustness in their profitability.

Risks

Price of the preferred stocks is not low for no reason. Synchrony preferred stocks are rated as speculative grade investment by both S&P and Fitch Ratings. This is mostly due to concentrated product portfolio in what is a volatile product. In addition, since Synchrony is distributing its credit cards through a portfolio of standard brick and mortar and online retailers, any bankruptcies among them could cascade and impact the size of its lending portfolio and thus earning power.

Source Fitch Ratings

This rating translates into a high historical default frequency, which is equal to 2.25% for this issue and its remaining maturity.

Source 2021 Transition and Default Studies, Fitch

For more on Fitch analysis of Synchrony, please refer to this link.

Assessment

In order to estimate the soundness of this investment, I used the above shown cumulative default rates, and I calculated the internal rate of returns for different call date scenarios. As a benchmark, I used current implied SP 500 index return. Each year, cash flow was corrected by multiplying it with cumulative survivor probability (1 – cumulative default probability), to obtain risk adjusted future cash flows. The standard IRR formula from Excel was used to calculate IRRs for alternative horizons.

Figure below show how nominal and risk adjusted IRR compare to the market implied yield of 8.95% at the price I initiated my position.

In the most optimistic case of November 2024 redemption, investment at these levels would imply a return at CAGR of 27.7%, for a diversified portfolio this is equivalent to 25.64%. Implied yield is becoming close to equal to market index implied yield only if holding period of 10 years is assumed.

At current (November 19, 2022), the above table would show the following values:

Here, a risk adjusted holding period of 10 years is a less rewarding option than holding a diversified market index.

Summary

I purchase Synchrony Financial preferred shares after this analysis, as it implies a yield on par with my portfolios historical returns in case it’s redeemed between years 2024 and 2025. I own common stock of Synchrony Financial, and I am confident that its earning power will remain stable in the upcoming half decade, providing enough self generated capital to meet regulatory demands and continue its shareholder return policy. This is a small part of my current portfolio, namely because I find it expensive to invest in USD, having the majority of my income and savings in EUR. Otherwise, this issue warrants a return on par of what I would demand from my average risk equivalent holding over the 3-year period.

Disclaimer and kind request

Before you take any actions based on this article, remember, you are trusting an analysis of an anonymous person. However, if you like it, and you think it makes sense, you can always support it by giving me a tip. Writing is something I do in my spare time, appart from full time job, and as anyone I would react to positive incetives.

In any case, it does not hurt to subscribe. It hurts me if you don’t 😇

An in case that you find this not worthy of subscribtion, at least comment.

Best of luck to all of us! 🍀

Warning to whomever is reading this, this thesis is no longer valid as Synchrony intends to IPO an additional series of preferred shares. Probability of early recall is low now. Dividend yield is attractive still.