1. China Mobile: Good Business Vs. Bad Politics

Summary

China Mobile is the largest mobile network provider per number of subscribers and the operator of the largest 5G network in the world.

For the past two years, its share price was under negative influence of the USA and China trade war and Executive order banning US investments in specific companies.

Due to current political situation, it is difficult for US and EU investors to buy or sell China Mobile shares.

China mobile still remains a profitable, growing business that is significantly undervalued.

Investment Thesis

While for China Mobile Limited, or CHL, the past year was exemplary and marked by some early successes in profiting from 5G implementation, the same period was marked by great political turmoil in US and EU vs. China relations that affected its share price negatively. The presidential order which had it forcibly put out of hands from US investors, and EU sanctions which put a temporary halt on trading with CHL shares, have led to major sell offs from western stockholders. However, if one could look beyond the circumstances of current global political plays, CHL is looking like a rare bargain opportunity in today's market. Debt free and with abundance of cash, it is ready to collect on past few years in investing in largest global 5G network in operation.

Business overview

CHL is majority state owned wireless telecommunications provider in China. It employs almost half a million people, servicing a customer base of 950 million. As a part of their transformation from a pure telecommunication company, the share of data services in their revenue stream has increased over time. Apart from substitution of voice, SMS and MMS services revenue with data transfer revenue, CHL has also worked on finding other service offerings for its customers. Services such are MIGU video (video streaming platform), and-Wallet (mobile payment solutions) and smart home have managed to open other sources of revenues from existing customers.

(Source: Author's Calculations)

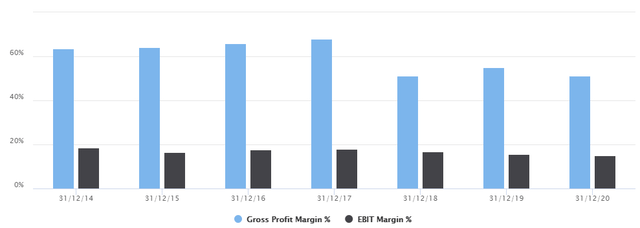

It should be noted that revenue in CHL was always under pressure from the government and plans to turn China into a digital powerhouse. Under this plan, pricing of it services was always capped. This has reflected in reduced gross and operating margins. Added to that, costs of expanding the 5G network also had their impact through increased amortization of capital expenditures.

(Source: Author's Calculations)

Recent developments

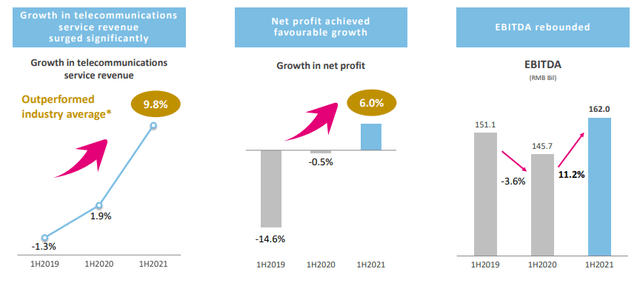

The last twelve months were anything but remarkable for CHL as a business. While its revenue growth was temporarily interrupted due to Covid-19 introduced lockdown measures, CHL has achieved record business growth in this year. This growth was partially driven by recuperation of lost revenue, but also by successful increase of alternative revenue streams. What also stand out is that for the first time in the last few years, average revenue per customer has actually increased.

(Source: Company presentation)

As a consequence of these results, half-year dividend was increased by 6.5%, resulting in total trailing dividend yield of 7.06%.

(Source: Company presentation)

What is worth noting is that CHL will issue new shares on Shangai stock exchange. As a part of this IPO, CHL will aim to collect CNY 59 billion, issuing no more than 965 million shares (4.7% of current shares outstanding). This Officially, motivation for this is to finance further expansion of their 5G network in mainland China. In my opinion, this is more of a marketing move and should not affect the future operation of CHL in any significant way. As I will show in intrinsic valuation, CHL currently has roughly CNY 530 billion in cash and investments, and are not in a dire need for additional funds for future growth.

However, all these results mean little when compared to the political games between the USA and EU on one side and China on the other. Since CHL was put on a list of companies involved in military programs, the exodus of institutional investors has begun, while countless individual investors were left to find their way out of locked assets. This oversupply pressure led to significant price decrease, with price finally stabilasing in last few months.

Long-term prospects

If it were not for the political obstructions, talking about the prospects of CHL, given the current price, would not have felt as bittersweet. Although extraordinary growth was achieved in the last 12 months, one should not expect it to last for too long. In my assumptions, I would allow for one year more of more than average growth due to higher average revenue 5G users replacing existing 4G users and further expansion is made in other service areas. After that, I would only assume that CHL returns to the standard operating model of growth at the pace of inflation and risk-free rate with stable margins, whilst maintaining its slight competitive advantage due to its sheer size and economies of scale. Future could hold more for CHL if any of its initiatives such as digital wallet or MIGU video manage to expand from being more than niche products on Chinese market. However, for the purpose of this valuation, conservative assumptions are enough to showcase the extent that political actions can have on share price.

Intrinsic Valuation Assumptions and Considerations

To calculate the fair value of CHL and convert its narrative into numbers, I used a three-stage discounted free cash flow model (growth due to roll out of 5G services, growth slowdown due to government pressures, and stable growth in perpetuity). The company's operating cash flows were valued as a going concern and discounted back at an estimated cost of capital. Cash and cash equivalents and the value of minority holdings were added back, while the market value of capital leases (treated as debt), minority interests and value of outstanding options were subtracted out to arrive at a total value of equity. Total equity value was then divided by the current total number of shares outstanding to obtain a fair value per share.

The following are the assumptions I used in the intrinsic value calculation for them:

Revenue growth

I assumed that the consolidated revenue will increase for 4% in next year, with further substitution of 4G vs. 5G customers and expansion of new services. After that, I assume that over the next five years their revenue grow only at the pace of the Chinese economy, i.e. it will grow according to the current risk-free rate. In the last stage, growth will still be tied to risk-free rate, however this rate is based on my assumption that it will revert to its 10-year historical average. This assumption will also be subject to simulations, in order to measure the sensitivity of my forecasts.

Target operating margins

CHL reported an operating margin of close to 14.24%. After I converted their capital leases to debt, I corrected this value to 16.5%. Nevertheless, I assumed that as of next year, operating margin will be 15% and that it will remain on that level in the future. This is just slightly below the global average for wireless telecommunication companies of 15.08%.

Reinvestment assumptions

Reinvestment needs are measured through the sales/capital ratio that includes R&D costs, sales and marketing costs needed to maintain and grow their revenue, and traditional capex. Based on five years of history, I normalized the reinvestment needs and calculated the value of 1.21 for sales/capital ratio.

With these assumptions, I assumed average ROIC over the 10-year period of 12.77%, while its average cost of capital value over this period was 6.58%.

Cost of capital

For cost of capital, I estimated cost of equity from the market-implied equity risk premium and I added a regional risk spread (based on CDS spreads) based on where revenues were earned. In the case of CHL, because 95% of the revenue is generated within mainland China, I decided to treat it as a fully Chinese company. Next, I used a bottom-up business beta from Telecom services companies and Telecom equipment providers in global markets and levered the beta to CHL's own adjusted debt/equity ratio. Multiplying the equity risk premium by the computed beta and adding it to the risk-free rate sums to a total cost of equity. The estimation was performed using September 05, 2021, values.

(Source: Author's Calculations)

Based on the current A1 rating from Moody's, I calculated the present value of capital leases, which I treated as debt. Cost of capital was then calculated as a weighted average of cost of equity and cost of debt, using market values of equity and debt to calculate relative weights.

(Source: Author's Calculations)

Terminal cash flow value

For value of the terminal cash flow, the following assumptions we used:

(Source: Author's Calculations)

I assumed that CHL will grow with the risk-free rate in perpetuity and that its return on capital will be higher than its cost of capital, which is a sensible assumption for a mature company of this size with a dominant position in its home market. Since my terminal value is sensitive to the choice I made regarding the future risk-free rate, sensitivity of my valuation will be tested to this in the final step (cost of capital and return on capital were also treated as a function of risk-free rate).

Valuation results

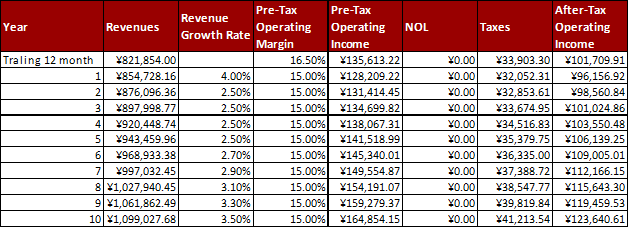

Values projected and discounted by these assumptions are as follows:

(Source: Author's Calculations)

As I mentioned, I kept the EBIT margin almost constant throughout the analyzed period. After next year, I would assume that the revenue will grow at the level of the current risk-free rate and just slightly above forecasted inflation rate for this period. After that, revenue will start to grow according to my expectation of risk-free rates reverting to the level of their mean in the prior decade. In my later simulations, I have tested the sensitivity of my valuation to this assumption.

Over the whole period, I assumed stable capital needs. This is in line with previous years investments practice in the past five years.

(Source: Author's Calculations)

Using the forecasted free cash flow for equity and calculated cost of capital, I calculated the present value of operating assets.

(Source: Author's Calculations)

Adding back the available cash and cash equivalents, and subtracting the value of debt, value of issued equity options and revalued cost of acquisition based on my estimate of fair price, the present value of CHL's equity is CNY 2.251.029 million. Using the current share count, this leaves us with a value of close to CAD 109.94 per share (or HKD 131.93).

(Source: Author's Calculations)

Furthermore, in order to mitigate the effect of potential calculation error and error in my assumptions, 10,000 simulations were run. This allowed for variability around assumptions risk-free rate after year 10 (using normal distribution around assumed 3.5% with 0.5% standard deviation) and terminal operating margin (using normal distribution around assumed 15.00% with 0.5% standard deviation). Note that the risk-free rate after year 10 affects both my perpetual growth rate and cost of capital after year 10.

(Source: Author's Calculations)

This results in a median present value per one share of CNY 109.6. However, even with all scenarios applied, the fifth percentile of the produced result distribution is close to CAD 102.9, which makes this forecast quite robust to future risk-free rate developments.

(Source: Author's Calculations)

At this stage, I usually try to input a set of assumptions in my calculation that would result in equaling the fair value I calculate with current market price. This time I will omit this part since it would require me to assume negative growth rates from this day forward, double less operating margins and perpetual decrease. However, this does not fit the narrative of CHL, nor any dominant wireless telecommunication company.

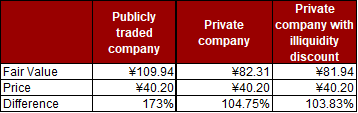

The only path I saw reasonable to explore is what would happen if I converted CHL to private company (since I can't sell it, it is private in my eyes). For a private company valuation, I would use total beta of 2.12, instead of industry levered beta. This would increase my cost of capital to 13.73% from initially used 5.98%, and with all else unchanged result in a value of CNY 82.31.

On top of this, I then added an illiquidity discount calculated based on fundamental data. Due to CHL size, this discount is 0.45%, and with this I could arrive to the fair value of CNY 81.94.

Finally we are left with these results:

(Source: Author's Calculations)

Here is another important information that should be kept in mind. At the current price of CNY 40.2 for one share, you would get CNY 24.2 in cash and cash equivalents, short term investments and trading securities held by CHL. The difference which you pay is the price the business defined by the market right now.

Risks

Investing in CHL is tied to several risks, most of which are not tied to the company itself.

First and foremost, I am not a legal expert, and I can talk only from my personal experience as an EU investor. Since I have invested in CHL in December 2020, actions taken by the USA and EU governments have prevented me from selling my shares at this moment, even if I wanted to. I invest with a long term horizon, and I believe that it is more probable that these sanctions will be relaxed in the period of next five years, then that further worsening of international relations will occur. Nevertheless, prolonged sanctions, beyond one investment horizon, could cause significant complications and additional costs in closing this position in due time.

Political actions may lead to force sales of individual holdings under unfavorable terms either because foreign listings are being discontinued, as in the case of ADR's on NYSE, or simply by legally enforcing the sale for certain foreign investors.

Currently, owners of CHL still receive semiannual dividend payments. This also, could be obstructed if political will existed.

However, what is of most relevance for me is sensitivity of potential returns to CNY exchange rate. Significant depreciation of yuan could effectively wipe out significant part of potential investment return. In the same time, given the calculated undervaluation of CHL and growing importance of CNY as world reserve currency, this event is both unlikely, and it should not result in loss of principal investment.

Summary

Even though CHL is not a risky company by itself, circumstances have turned it into a risky investment. But, one should keep not forget certain inevitable facts that will over time steer the price of CHL toward its fair value. First, China and Asia will continue to progress and catch up with the rest of developed world over time. Second, CHL will remain an integral part of the infrastructure of the society driven by digital revolution and grow with it. And third, politics change over time and in unforeseeable directions, but in the long run societies progress and cooperate.

I don't take sides in political disputes, because perceptions of right and wrong are rarely governed by objective facts or reason. But I will use objectivity to shelter myself from making irrational decisions on my own. In case of CHL, I will hold it for years to come and if I was not prevented, I would invest more.