15. Topicus value shortcut, Terravest source of maintenance capex and cash available for distribution

Some interesting data from my latest analyses

Topicus value shortcut update

Recently, I have written about what I found to be a good proxy for determining a possible IRR for investment in Topicus at current price levels. As all proxies, it is just a quick measure to signal if something is significantly mispriced or not. Personally, I am an avid believer in that value of a company is present value of its discounted cashflow’s, but building and updating these models takes times and I do it only periodically for companies I am comfortable having as my holdings.

Proxies serve a different purpose. They are just a quick measure to signal if something is significantly miss priced or not. As Topicus has released its December 2023 results, I spent a few minutes to update the information on the data I deem to be a relevant measure of the business quality, and proxy for its implied rate of return going forward.

The following figures show the development of Topicus as a business-tough income statement (in EUR). So far, revenues have grown in line with a long term compounded average, and there are no significant indications of this slowing down or that the structure of revenue sources is changing.

As for the organic revenue (better visible in the separate graph), Topicus slowed down its growth in real terms during 2022, when across its operating markets it experienced inflation of 6-8%. Interestingly enough, it achieved organic growth of 7% which translated to 4% real growth using December CPI for EU as benchmark.

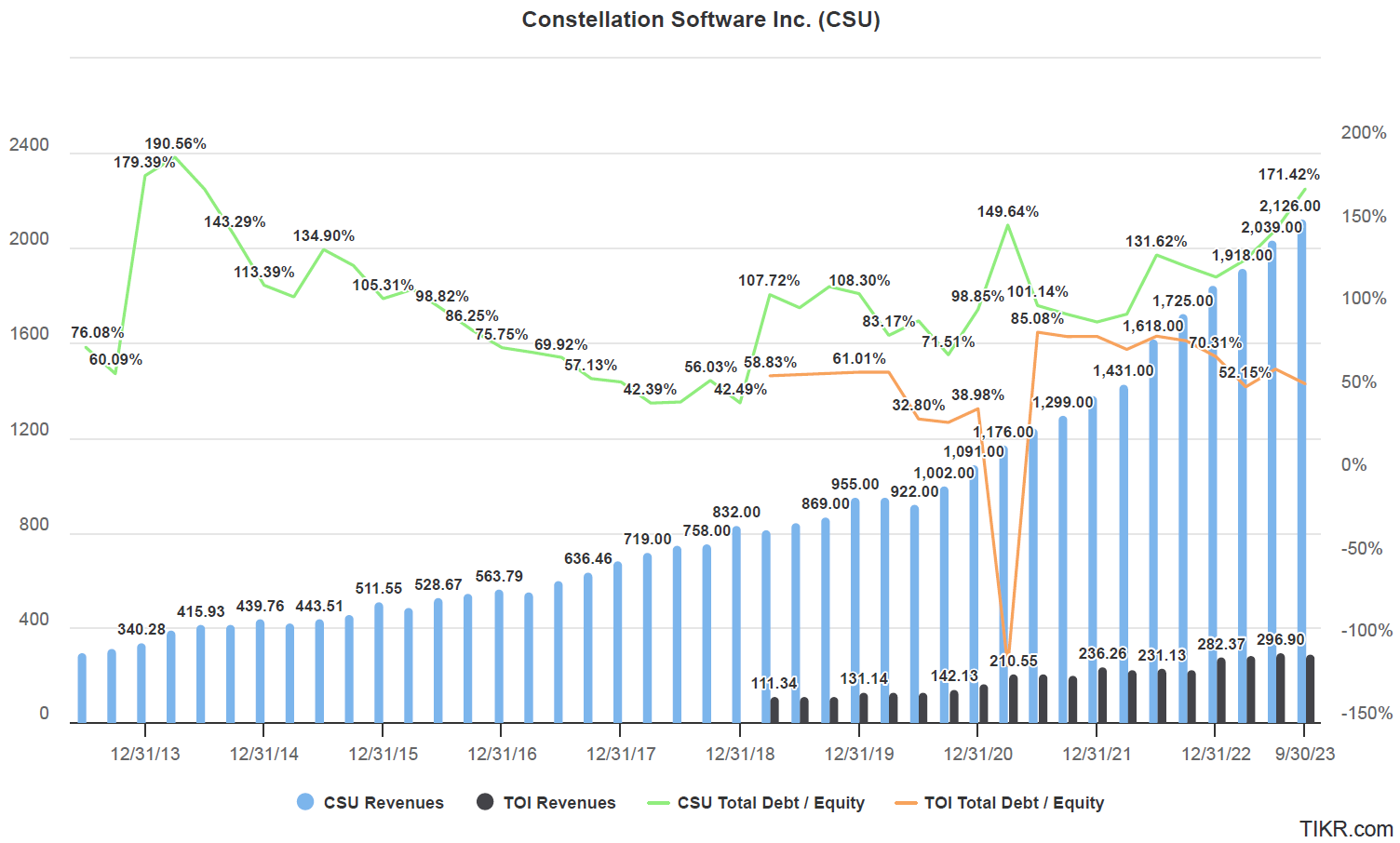

For those who are long-term investors in Constellation, ROIC+Org% is a well-known metric that was once embedded into the CSU internal performance assessment scheme. It is still a good proxy for initial shareholder returns (note: those who provided initial equity). Maintaining this rate above 20% is something only a few companies can achieve without excessive leverage. In the case of Topicus, decay is visible, and some midterm level of 25% can be expected.

Topicus is currently in September 2013 of Constellation Software history, measured through total revenue. However, it spent good part of 2023 reducing it’s debt (part of it also being interest free Constellation debt) to a level Constellation did not have in a decade. It is reasonable to assume that 2024 will bring a new debt facility to be used to leverage M&A and probably increase ROIC a bit.

As for the organic revenue, my suspicion is that this is actually attributable to Topicus (Topicus.com owns Topicus and TSS). At least based on my account, TSS acquired 14 companies in the Netherlands in 2021, 2022 and 2023 that brought in 65-75 million of revenue. But figures below show a growth of 150 million in the Netherlands alone. At the same time, my data shows a total of 45 acquisitions in the rest of the world for total revenues acquired of close to 300 million. My revenue estimates are not perfect, but directionally they seem to support the assumption that Topicus actually grows their business apart from TSS acquisitions. Something Constellation has always claimed that they did better than any other business unit in the group.

Finally, using latest EUR CAD FX rate, share count and market price, coupled with December financial statements data, results in a proxy for an implied rate of return of 9.33%. Some 10% relatively less than last time, but still above what I would estimate to be a cost of capital for Topicus (you assume at least some protection to specific business risk).

The last measure I follow, albeit not so popular in the eyes of many, is the efficiency of capital allocation and capital structure development.

Understanding the importance of intangible assets in the case of Topicus is a necessary, as they are a major source of cash flow that is not observable at a first glance. Capital employed (total equity plus interest-bearing debt net of cash plus accumulated intangibles amortization), has grown to almost 1.3 billion EUR. It doubled in less than 3 years (2 years and 3 quarters to be precise).

At the same time, nothing out of the ordinary is happening with the prices paid for acquisitions. Measured through sales to capital employed ration, it is as stable as it can be.

For conclusion, Topicus is operating and growing as one would hope, but not dare to expect for many other companies out there.

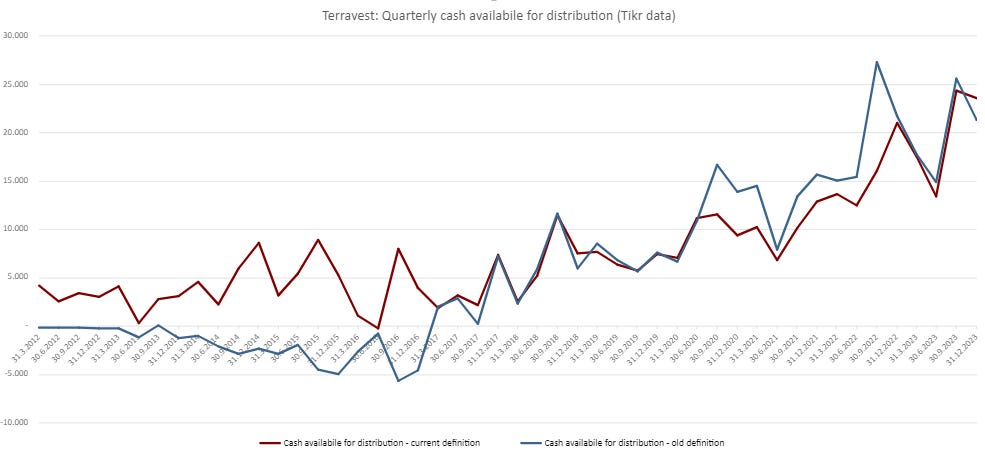

Terravest source of maintenance capex and cash available for distribution

I have been reading into Terravest for more than a year, but the recent Plural Investing Group report from 2024 is making me rethink how I view their capital allocation strategy. Put shortly, I underestimated how much of capital is generated from restructuring acquired companies. Compared to CSU and Topicus, Terravest seems to be a bit more brutal towards its acquisitions, but results are interesting.

Based on TIKR data, I was able to recreate their measure of cash available for distribution (cash they can use for dividend payments, acquisitions, debt repayments, and to support their leverage).

But dig a little further, and you can see that a large part of their maintenance capex comes from gains in restructuring (sale of redundant facilities of acquired companies). During their history measured from March 2012, a total of 70 million was spent as maintenance capex, but sale of property, plant and equipment produced 49 million of funds (70% of cumulative maintenance capex).

I will share my valuation once I think it is stable enough.

Disclaimer and kind request

Before you take any actions based on this article, remember, you are trusting an experimental analysis of an anonymous person. However, if you like it, and you think it makes sense, feel free to support my writing which I do in my spare time, while working a full time job. If anything you pick up from my substack or Twitter account results in you earning a reasonable profit, keep the karma going. Subscribe, even for a month.

In any case, it does not hurt to subscribe, share this article or comment. It hurts me if you don’t 😇

Or just share your best idea you can quantify with me.

Best of luck to all of us! 🍀