19. Pinetree NAV, tracker and valuation based on Q2 2024

Short update on Pinetree portfolio and the quick take on Trubridge - their currently and historically largest holding by cost basis

Disclaimer: I own Pinetree.

But not nearly enough. I made a mistake in my initial position sizing and it’s almost not relevant in my overall portfolio. Nevertheless, following Pinetree is similar to a free investment course, so I will continue following it closely and posting my notes on it (in hope that new safe buying opportunity occurs).

Purpose of this note is just to provide brief overview of the current status of Pinetree before their Q3 release to hold myself accountable. For more details on how I view Pinetree and why I consider some parts of their financial disclosures more relevant than others, please see my other note - 17. Pinetree Holding: Special situations vehicle of Leonard family.

Pinetree Q2 update

As I noted in my previous note, story of Pinetree is the story of how existing loss carryforwards can be used as efficiently as possible in order to benefit existing shareholders. By efficiency, I primarily refer to speed in which they can be used to realize capital gains, without diluting effect of raising additional capital to achieve those capital gains. Dilution can be a good thing, like the time Shezad was brought in thanks to it, but should not occur only for the purpose of having more funds available. So far there is no indication that this will happen. For the matter of fact, Shezah is not even there anymore (although he should be back any time, since his tenure at Bravura Solutions has ended).

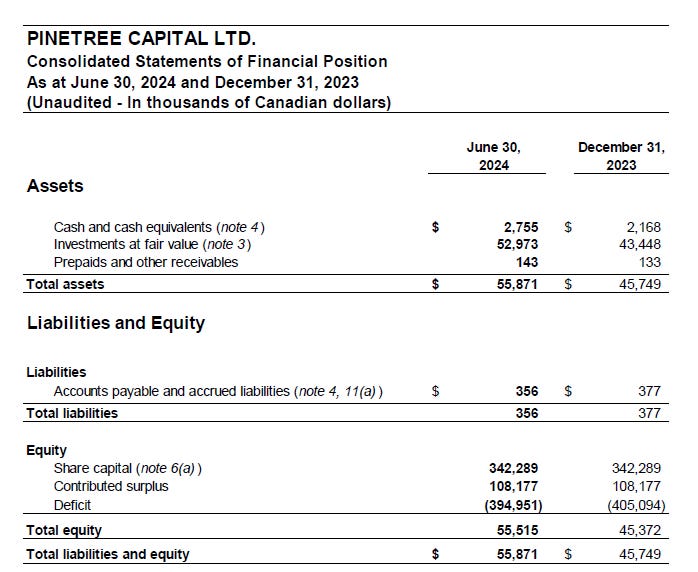

As of the last quarter loss carry forwards that can offset future capital gains has been reduced to CAD 394 million.

There is no certain way to value Pinetree. What I consider as reasonable metrices are NAV measured through cost and fair value, paired with DCF of alternative levels of normalized earnings until deficit is fully utilized.

If you remember, in my valuation attempt I used this deficit as a budget for estimating remaining life of Pinetree. Speed of utilization of this deficit would determine the number of years over which I would discount some estimated amounts of normalized earnings, both realized and unrealized, since under my valuation assumptions, once deficit is fully used, Pinetree will be dissolved. This of course is only a speculative assumption on my side.

Back then I provided following expectation of deficit development (zoom in):

Based on my then normalized earnings assumption, deficit should have been around CAD 402 million by now. However, mostly unrealized gain in the Q1 2024 of CAD 11 million has eaten up a larger chunk of it than I expected.

Equivalent of the beautiful table above would now look like this:

Shown as a figure:

Changing the assumptions for the normalized yield, following scenario values can be produced (scenario of 15% equates cumulative realised and normalised realized yield over the period of 4.25 years).

Compared to my initial notes, adjusted yield changed by 100 basis points due to high unrealized gains in Q1 2024. However, this was a period of market recovery and one should not take it away from Pinetree. They started in the normal market conditions, experienced two downturns and are going back to normal again. Market cycle is complete for them.

Apart from the mentioned scenario, one is free to choose the scenario based on his expectations from the table below.

To make it clear, market will never value Pinetree like this. Simply, it’s a risky thing to do since there is always a risk of failed concentrated investment removing years of positive results and track record. If anything, the fair values indicated above can give you the insight into potential IRR you could expect if any of the above mentioned scenarios realizes over the period of Pinetree existence (divide the cost of equity with % to value for a quick measure).

Measured though NAV by any definition, Pinetree is currently priced above them.

Using 30.09.2024 values

Using 18.10.2024 values

My personal threshold for investing in it is some level close to the cost value at the moment of investment.

As for their realised transaction (or partially realised transactions in case of Sygnity), Pinetree continues to close their positions at 40% CAGR.

But more importantly, they continue to turn their portfolio and utilise their capital gains buffer. The fact that they are selling their Sygnity and Topicus holdings gradually, indicates that there is some process behind their operation and a level of ruthlessness when it comes to their holdings. I hold both Sygnity and Topicus in my portfolio, but I am not considering selling either of them even if I consider Sygnity slightly overvalued and Topicus at fair value on a probability weighted outcome basis.

Notable absences from their portfolio are Trucontext, sold for realized gain of CAD 1,007 thousand, or 154% return over the holding period (resulting in 36% CAGR), Sapiens sold for realized gain of CAD 1,665 thousand, or 70% return over the holding period (resulting in 36% CAGR). Horizons High Interest Savings ETF position of 2,454 thousand was eliminated probably for no significant loss. All these fund have gone into two new positions. One of them is now the largest position in Pinetree’s portfolio - Trubridge.

Other is unknown and all information that was disclosed was that it is Germany- Healthcare Software company. Last time similar description company was in their portfolio was in 2023, when during the first quarter, position was closed in its entirety.

Then, Compugroup Medical, was sold after roughly a year of being bought. I have very little insight into this company, but it seems that understanding the intricacies of this business, might come in as a useful knowledge given latest market reactions.

With no other evidence, I am only left to speculate that Pinetree again invested into Compugroup. But more relevant for Pinetree, focus should be on TruBridge.

Trubridge is an interesting investment for Pinetree. By my measures, it their largest position that they cumulated in such relatively short time.

First shares were purchased at late January this year, with majority of the current holding being acquired in May at about USD 7.8 per share.

What is interesting about this investment is also that similar to Bravura Solutions, Pinetree is accompanied by like-minded investors seeking to create shareholder value, namely L6 Holdings and Strikwerda family.

Together with them, existing management (CEO, CFO, COO, CTO and many others) have purchased quite a lot of shares since the beginning of the year.

Over past month or so I have been attempting to put a value, or range of values on Trubridge in order to understand what Pinetree sees in them from investment point of view. I will release my notes on them in next few days, but before raising expectations, have in mind that I am not able to identify exact outcome of the Trubridge transformation confidently at this point. Unlike in Bravura where plan was laid out in a more precise way, and activist investors had a seat at the executive board, here only partial mentions of the end state are provided. This is precisely why I invested in Pinetree, as I am aware that I lack the know-how to assess the value creative results of distressed business transformation activities. But, without trying to figure it out, I will never learn.

So, let’s follow true and hopefully bridge across the gap. My notes on Trubridge will be published in the next days. Hopefully comments collected on them guide us all close to the correct pathway in the see of possible scenarios.

Disclaimer and kind request

Before you take any actions based on this article, remember, you are trusting an experimental analysis of an anonymous person. However, if you like it, and you think it makes sense, feel free to support my writing which I do in my spare time, while working a full-time job.

If anything you pick up from my substack or Twitter account results in you earning a reasonable profit, or avoiding unreasonable loss, keep the karma going. Subscribe, even for a month. Even years after you have read something from me, based on realized experience.

In any case, it does not hurt to subscribe, share this article or comment. It hurts me if you don’t 😇

Or just share your best idea you can quantify with me.

Best of luck to all of us! 🍀

"existing management (CEO, CFO, COO, CTO and many others) have purchased quite a lot of shares since the beginning of the year."

Where are you seeing this? because I have to disagree.

Very helpful. Thank you for sharing.